March 04, 2026

March 04, 2026The 2025 Düsseldorf International Medical Equipment Exhibition Opens

On the final trading day of the week, the broader market indices continued their upward trajectory in the afternoon session, while the semiconductor industry chain maintained its strong momentum. Approaching the market close, the Upstream Semiconductor Equipment ETF (561980) rose by 1.46%. Among its constituent stocks, Jingyi Equipment surged 8.85%; Tianyue Advanced, Shanghai Xinyang, and Zhongke Feice each gained over 5%; and numerous other stocks—including Anji Technology, Topping Technologies, Piotech, and Naura Technology—saw significant rallies.

In terms of market news, the domestic lithography machine sector has achieved another critical breakthrough. Shanghai Xinshang Micro-Equipment’s first independently developed 350nm stepper lithography machine (Model AST6200) has successfully completed factory debugging and final acceptance testing, and has now been officially shipped to the client's site.

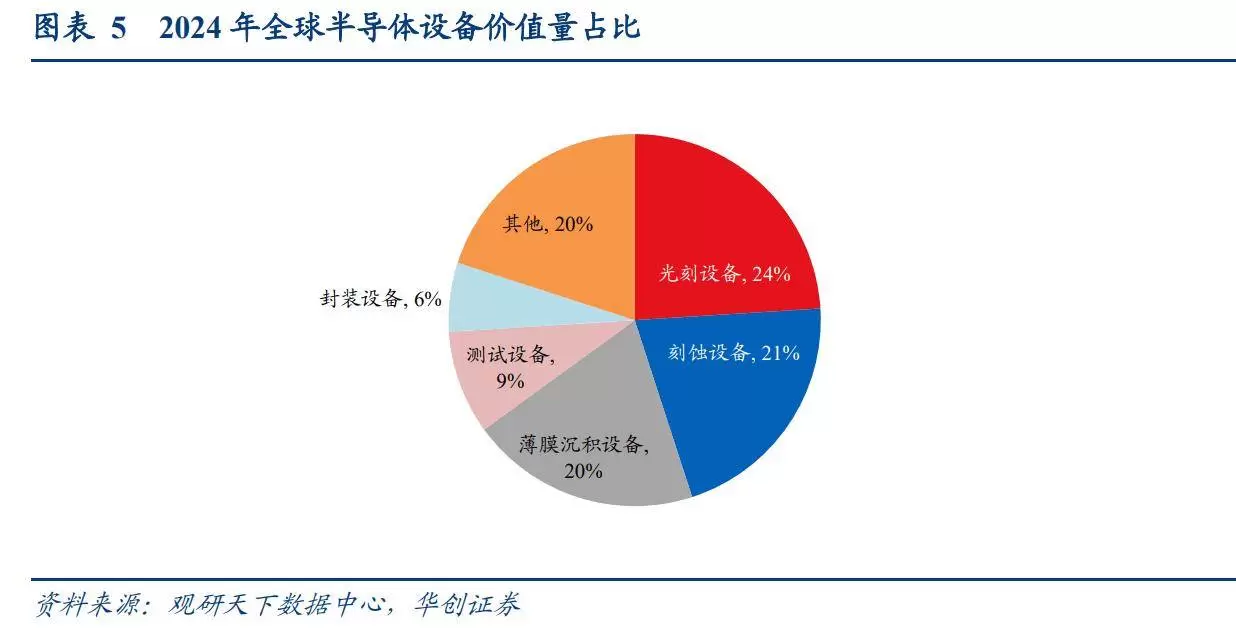

From the perspective of the industry chain, lithography machines represent an extremely high-value segment and constitute the largest product category by market share within the broader semiconductor equipment sector.

According to data from LeadLeo Research Institute, approximately 20%–30% of a wafer fab's capital expenditure is allocated to facility construction, while the remaining 70%–80% is invested in equipment. In 2024, global semiconductor equipment sales are projected to reach approximately $109 billion; among the core equipment categories—namely lithography, etching, and thin-film deposition—lithography machines lead the pack with a market share of roughly 24%.

Looking ahead to 2025, the latest research report from DIGITIMES indicates that global wafer foundry revenue is expected to reach US$199.4 billion this year—a year-on-year increase of over 25%. Furthermore, the Compound Annual Growth Rate (CAGR) for the 2025–2030 period is projected to reach 14.3%, positioning the sector as the most significant driving force behind the semiconductor industry's economic upturn.

In its latest global fab forecast report, SEMI also noted that global spending on front-end fab equipment is expected to rise by 2% year-on-year in 2025, reaching US$110 billion. This marks the sixth consecutive year of growth since 2020. Regionally, China is expected to maintain its leading position globally in semiconductor equipment spending, with expenditures projected to reach US$38 billion this year.

In light of this, Industrial Securities suggests that 2024 will be led by lithography, while the advancement and verification of domestic equipment for advanced process nodes continue to make steady progress. Over the next three years, "capacity expansion in advanced processes" is likely to emerge as the central theme driving the push for technological self-reliance and control.

Among market participants, the Semiconductor Equipment ETF (561980) has garnered significant attention; it tracks the CSI Semiconductor Index, in which the three sectors of semiconductor equipment, materials, and integrated circuit design collectively account for over 90% of the index's composition. The top ten holdings—including AMEC, Naura Technology, Cambricon, SMIC, and Hygon Information—make up over 78% of the portfolio. Given the index's notable market elasticity, it offers a potential avenue for investors to position themselves for the upcoming semiconductor up-cycle and to capitalize on the growth dividends generated by the industry's drive toward technological self-reliance.

Source: Sohu News

March 04, 2026

March 04, 2026 March 04, 2026

March 04, 2026 March 02, 2026

March 02, 2026 April 07, 2026

April 07, 2026Encountering problems or challenges? Please contact us!